The Weil European Distress Index

The latest Weil European Distress Index (WEDI), a closely watched early indicator of corporate distress and default risk, shows that corporate distress across Europe rose in the second quarter of 2026, reversing the modest easing recorded earlier in the year.

Distress increased across every market measured between February and May 2026, leaving overall distress above its long-run average. Rather than entering a period of falling inflation and easing monetary policy, corporates now face renewed uncertainty around energy costs, inflation and refinancing conditions, adding to an already fragile position. Profitability has become the single largest driver of distress across Europe, reflecting softer demand, elevated operating costs and growing uncertainty around future trading conditions.

Sector Spotlight

- Retail and Consumer Goods: The most distressed sector in Europe by a clear margin, with distress rising sharply on both the quarter and the year. On a rolling basis, distress reached its highest level since the global financial crisis in the latest quarter. Profitability remains the key pressure point, alongside a broader squeeze on liquidity, investment and valuation, as weak consumer confidence, softer discretionary spending and rising operating costs weigh on activity. As a result, the sector remains highly exposed to any renewed squeeze on energy and transport costs.

- Industrials: The second-most distressed sector, with pressures rising on the quarter, though distress remains lower than a year ago. The increase suggests the tentative stabilisation seen earlier in 2026 remains fragile. Weak investment conditions, subdued demand and a challenging export environment continue to weigh on manufacturers. The Iran conflict has compounded these pressures, raising uncertainty around energy costs, supply chains and global demand, and leaving energy-intensive businesses particularly exposed.

- Infrastructure, Utilities and Power: Now the third-most distressed sector, having recorded one of the sharpest deteriorations in the index. Growing pressure on investment, liquidity and risk points to more challenging financing conditions and project economics, while delayed procurement decisions and uncertainty around energy markets continue to weigh on capital-intensive operators.

- Travel, Leisure and Hospitality: A sector to watch. While distress remains below its long-run average, it has risen sharply on both the quarter and the year, marking a clear change in momentum. Liquidity and profitability are now the key pressure points, reflecting higher wage costs, weaker consumer confidence and greater sensitivity to geopolitical disruption. As higher fuel costs feed through to company results, distress is expected to continue rising in the months ahead.

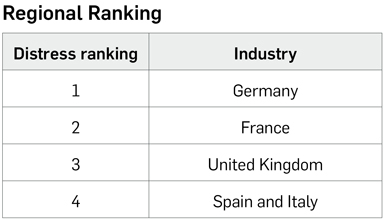

Regional Spotlight

- Germany: Remains the most distressed market in Europe, with conditions still elevated despite some improvement compared with last year. Distress rose again on the quarter, driven by profitability, liquidity and investment. Germany’s reliance on manufacturing, exports and energy-intensive industry leaves it particularly exposed to weaker demand and higher input costs, while corporate insolvencies, at their highest level since 2014 in 2025, continue to underline a fragile backdrop.

- France: Distress has risen again in 2026, leaving France as the second-most distressed market and the only market in the WEDI where distress is higher than a year ago. This is the clearest deterioration story among Europe’s major economies. Pressure remains concentrated in profitability, liquidity and investment, while valuation metrics have deteriorated markedly. Corporate bankruptcies have reached their highest level since the early 1990s, underscoring an increasingly challenging backdrop for French businesses.

- United Kingdom: The third-most distressed market, with pressure spread across investment, liquidity and profitability. A softening labour market and persistent cost pressures continue to weigh on business confidence. The UK is particularly sensitive to the energy and interest-rate channels. The IMF recently cut its 2026 growth forecast from 1.3% to 0.8%, the largest downgrade among the markets covered by the index, reflecting the impact of the Iran war on energy costs and inflation.

- Spain & Italy: Remain the least distressed markets, with distress below the long-run average, though it has risen modestly since the start of the year. Increasingly, this is a story of divergence rather than shared resilience. Spain continues to outperform, supported by stronger domestic growth, while Italy faces a weaker outlook shaped by lower productivity, fiscal constraints and softer external demand. The rise across both markets reinforces the broader trend of pressure building across Europe.

Looking Ahead

As an early indicator of corporate distress and default rates, the WEDI’s message this quarter is less about where distress is highest, since the rankings are broadly unchanged, and more about the change in direction. After easing at the start of the year, distress is rising again across the board, and businesses are meeting a fresh energy shock from an already weakened starting point.

The tension to watch is between market sentiment and company fundamentals. Equity and credit markets have stayed comparatively calm, betting that the disruption from the war in Iran proves temporary and that policymakers can still support growth. The WEDI suggests the ground beneath is shifting, with profitability, liquidity and investment all deteriorating. Should inflation prove stickier, rate cuts arrive later or energy prices stay elevated for longer, the gap between resilient markets and weakening fundamentals may yet have to close, most acutely in the energy-intensive and consumer-facing sectors already carrying the most strain.

Andrew Wilkinson, Partner and Head of Weil’s London Restructuring practice, said:

“European businesses entered 2026 expecting operating conditions to improve gradually. Instead, the outlook has become more uncertain. Distress is now rising across every market we track, profitability has emerged as the biggest source of pressure and the prospect of lower interest rates looks less certain than it did at the start of the year.

One of the more striking features of the current environment is the disconnect between market sentiment and underlying company fundamentals. Equity markets have proved remarkably resilient and credit markets remain relatively stable, reflecting expectations that the disruption caused by the war in Iran will prove temporary and that policymakers will ultimately be able to support growth.

The WEDI points to a different picture beneath the surface. Many businesses are already absorbing higher energy and operating costs, while profitability, liquidity and investment continue to deteriorate. If inflation proves more persistent, interest rates remain higher for longer and energy prices take longer to normalise, markets may need to reprice those risks more fully.”

Contributor(s)

More from the Weil European Restructuring Blog

This website is maintained by Weil, Gotshal & Manges LLP in New York, NY © 2020 Weil, Gotshal & Manges LLP, All Rights Reserved. The contents of this website may contain attorney advertising under the laws of various states. Quotation with attribution is permitted. This publication is provided for general information purposes only and is not intended to cover every aspect of the purpose for the law. The information in this publication does not constitute the legal or other professional advice of Weil London or the authors. The views expressed in this publication reflect those of the authors and are not necessarily the views of Weil London or of its clients. These materials may contain attorney advertising. Prior results do not guarantee a similar outcome.